Originally published: July 2025 | Updated: December 2025 | Reviewed by Mary Conte

Naming both primary and contingent beneficiaries makes sure your assets end up where you want, even if your first choice can’t receive them.

These terms are crucial in estate planning for Central Florida residents who want to protect their loved ones and ease transitions during challenging times.

Understanding how these roles work can help reduce confusion and avoid unwanted legal issues.

A primary beneficiary is the first person or group in line to inherit from a will, retirement account, or life insurance policy. If that person can’t accept the assets—perhaps they’ve passed away or something else has happened—a contingent beneficiary is next in line.

This setup gives families peace of mind, knowing there’s a backup if life throws a curveball. It’s honestly more common than you’d think for things not to go as planned.

If you own property, life insurance, or investments, you’ll want to know these terms before making big decisions.

A beneficiary is the person or group who gets money or other assets from an estate, trust, or financial account after the original owner passes away.

Selecting beneficiaries is a crucial part of any estate plan, as it determines who will inherit assets, such as life insurance, IRAs, or living trusts.

You’ll find beneficiaries named in legal documents, such as wills, trusts, life insurance policies, and financial accounts. That person or group has the legal right to receive some or all of the listed assets.

There are two main types: primary beneficiaries (they’re first in line) and contingent beneficiaries, who step in if the primary can’t. Trustees and insurance companies follow these names when distributing benefits.

A beneficiary’s primary responsibility is to receive and utilize the assets as they see fit, unless a trust or specific instructions dictate otherwise. Selecting the right people helps ensure that your wishes are followed with less confusion and drama.

You can name beneficiaries for all sorts of assets and accounts. Common ones include:

For life insurance, the beneficiary receives the payout upon the insured person’s passing away. Retirement accounts allow you to name both primary and contingent beneficiaries, which helps assets bypass probate and makes the process clearer.

Trusts also utilize beneficiaries, and a trustee manages and distributes assets over time. This setup can provide you with more control and sometimes offer tax benefits. Many estate plans utilize a combination of these to ensure a smooth transition.

Florida law permits owners to designate whomever they choose as beneficiaries on financial accounts, life insurance policies, and estates. These designations typically supersede those in a will, so keeping your forms updated is crucial.

If you don’t name a beneficiary or if that person has died, the asset might end up in probate court. In Florida, assets left to a spouse get extra protection, and if you name a minor, a guardian or trust will handle their inheritance.

State law generally shields insurance death benefits and certain retirement accounts from creditors. Florida also recognizes payable-on-death and transfer-on-death designations, making it easier to pass on assets directly.

Safeguard your family’s future with a tailored estate plan from Conte Mollenhauer Law, P.A. Learn how a Florida trust can protect what matters most. Schedule your consultation today.

If you’re ready to get started, call us now!

Picking a primary beneficiary is a big step in estate planning. Whoever you name will be the first to get assets or benefits from your policy, account, or estate.

A primary beneficiary is the first in line to receive benefits if the account or policy owner passes away. This can be anyone you trust—a spouse, child, family member, close friend, or even a charity. Businesses and other legal entities can qualify, too.

In Central Florida, most people choose their immediate family, but some opt for friends or organizations they care about. The main thing is that the person or group is named and easily identifiable.

Use cases and include additional information such as birth dates or Social Security numbers.

This helps avoid mix-ups during claims. Clear identification makes it way easier for banks or insurers to locate and verify the right person.

Financial institutions and insurers in Florida allow you to update your beneficiary choices at any time. Keeping this information current is the only way to ensure your wishes are followed.

If your primary beneficiary dies before you do, they obviously can’t receive anything. Unless you’ve named a contingent beneficiary, the assets might go to your estate, which usually slows things down and can mean more taxes or court headaches.

Florida residents should review their beneficiary choices after significant life events, such as marriage, divorce, or the loss of a loved one. Updating designations right away helps prevent surprises.

Having backup beneficiaries helps keep your assets out of probate, a drawn-out and public process. Contingent beneficiaries are your safety net if the primary beneficiary hasn’t accepted the assets.

Some folks want to split assets between several people or groups, so they name more than one primary beneficiary. This is common for parents with multiple kids or anyone supporting different causes.

If you choose this route, you’ll need to decide how to allocate resources—by percentage or fixed amount. Here’s a simple example:

| Beneficiary Name | Share (%) |

| Spouse | 70 |

| Child | 30 |

This way, your wishes are spelled out. However, if one beneficiary cannot claim their share and you haven’t set up a backup, things can become complicated. Keep your designations up to date for smoother transfers.

A contingent beneficiary is your backup—they get the assets if the main beneficiary can’t. Understanding this helps protect your family, avoid delays, and ensure compliance with Florida law.

The contingent only receives assets if the primary can’t—maybe they’ve passed away or can’t accept the inheritance for some other reason. This often arises with life insurance, retirement accounts, and occasionally bank accounts.

Say you name your spouse as primary and your daughter as contingent. Your daughter only gets the benefit if your spouse isn’t alive when the claim happens.

Choosing a contingent means that someone you trust still receives the money if your first pick is unable to. This backup helps avoid probate and can expedite the process for your family.

One common mistake is skipping a contingent beneficiary altogether. If you leave this blank, your estate is open to problems and delays—assets might end up in probate, which nobody wants.

Some people name minors or others who can’t legally claim the inheritance, but forget to set up a trust or guardian.

That just adds hurdles. Another significant one: forgetting to update beneficiaries after life changes, such as divorce, marriage, or the birth of a child.

To avoid headaches, always use clear names, note relationships, and keep your paperwork up to date. Many don’t realize how crucial this is until something goes wrong. Naming the right contingent is just smart planning.

Florida law ensures that your property is distributed to the right person with no fuss. Listing a contingent beneficiary on your policies and accounts makes this a lot smoother.

If you don’t have a backup, and the primary isn’t available, state inheritance rules take over. That could mean your money goes to someone you didn’t choose, or it gets tied up for months.

A good backup plan also protects against things like joint deaths or sudden changes in your family.

For Central Florida residents, being specific about contingencies brings peace of mind and reduces legal headaches for your loved ones.

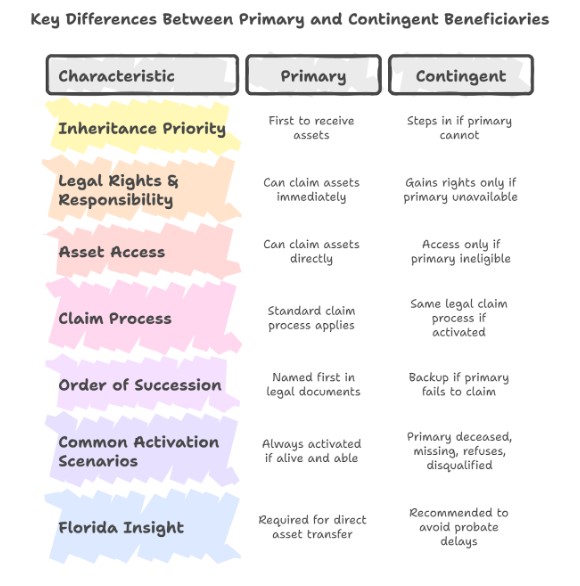

When deciding who will inherit your assets, it’s essential to understand the differences between primary and contingent beneficiaries. Your choices affect legal rights, who inherits first, and sometimes even taxes.

A primary beneficiary gets the legal right to assets first if you pass away. You can name them directly on life insurance, retirement accounts, or in your will.

A contingent beneficiary only gets assets if the primary beneficiary can’t. If the primary is deceased or can’t be found, the contingent steps in. Both have specific legal claims once it’s their turn.

Legal responsibilities include filing a claim and managing the associated paperwork. Sometimes beneficiaries owe taxes, depending on the asset and Florida law.

The order of succession outlines who inherits your assets and in what order. It’s essentially a roadmap for what happens to your belongings after you’re gone.

This order covers items such as insurance payouts, bank accounts, and investment portfolios. If a primary can take possession, the contingent gets nothing.

Legal professionals in Central Florida stress the importance of clearly naming both primary and contingent beneficiaries for every account or policy.

A contingent beneficiary only inherits if the primary is “unable,” which usually means the person has died, declines the inheritance, or is legally disqualified.

Common situations include:

In these cases, the contingent beneficiary becomes the legal heir. Financial advisors often recommend naming at least one contingent beneficiary to avoid having your assets tied up in probate.

| Category | Primary Beneficiary | Contingent Beneficiary |

| Inheritance Priority | First in line to receive assets upon your death | Steps are only if the primary cannot inherit |

| Legal Rights & Responsibility | Has the legal right to claim assets immediately | Gains legal rights only if the primary is deceased, missing, declines, or is disqualified |

| Asset Access | Can claim life insurance, bank accounts, and retirement funds directly | Can only access assets if the primary is no longer eligible or alive |

| Claim Process | Must file a claim, provide documentation, and may need to pay taxes depending on the asset | Follows the same legal claim process if activated |

| Order of Succession | Named first in wills, trusts, or policies | Listed as a backup to receive assets if the primary fails to claim |

| Common Activation Scenarios | N/A – always activated if alive and legally able | – Primary is deceased- Primary cannot be located- Primary refuses asset- Legal issues (e.g., divorce, crime) |

| Florida-Specific Insight | Naming a primary is required for direct asset transfer outside probate | Florida attorneys strongly recommend naming a contingent to avoid probate delays or confusion |

Florida estate planners emphasize the importance of naming both a primary and contingent beneficiary on every major account to protect your loved ones and keep your estate out of probate.

One person can’t be both a primary and a contingent beneficiary for the same asset at the same time. The roles are meant to be separate.

But the same person could be the primary on one account and the contingent on another. If there are multiple slots, someone might appear in both groups, possibly for different percentages.

It pays to review all your beneficiary designations to avoid mix-ups. After significant life changes, recheck to ensure your asset distribution still aligns with your desired goals.

Need help deciding between primary and contingent beneficiaries? Conte Mollenhauer Law, P.A., can walk you through every detail of your estate plan. Contact us to get started.

If you’re ready to get started, call us now!

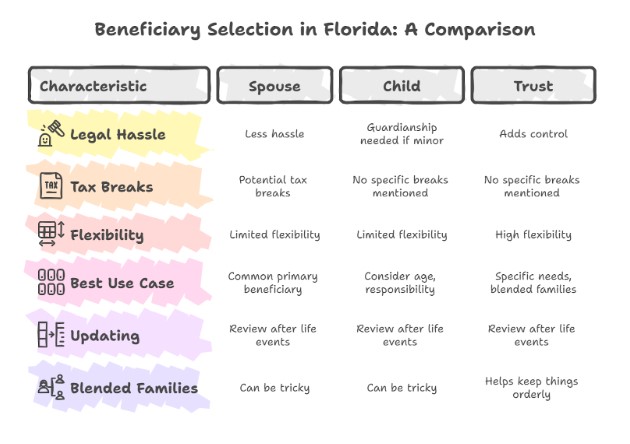

Choosing beneficiaries is a crucial aspect of any estate plan. Florida residents must balance their family needs, legal requirements, and personal wishes to ensure that assets end up in the right hands.

In Florida, spouses are typically the primary beneficiaries. Assets often pass to them with less legal hassle, and married couples may also receive some tax benefits.

If you name a spouse, spell out which accounts or assets they’ll receive. For kids, consider their age, financial responsibility, and whether they’ll inherit directly or through a trust.

Trusts add a layer of control. If you want assets used for a specific purpose, such as education, a trust can help. You can name family members, charities, or multiple heirs, and trusts are particularly useful for blended families.

Splitting assets among several beneficiaries can help maintain fairness and set clear expectations.

Florida law doesn’t let minors directly inherit most assets. A legal guardian or trust has to manage the inheritance until the child turns 18.

If you name a minor as a beneficiary, the probate court might appoint a guardian. That process can drag on and may not follow your wishes.

Setting up a trust sidesteps this issue. A trustee manages the money based on your instructions, and you can set up staggered payouts for things like school or healthcare. It’s a relief for parents and grandparents to know there’s a plan.

Big life events—marriage, divorce, births, deaths—should make you double-check your beneficiary designations. Old info can confuse or send assets to the wrong person.

In Florida, it’s wise to review estate documents every couple of years, or sooner if a significant event occurs. Employers and financial companies sometimes update their forms as well, so regular updates ensure accuracy.

As families and wishes change, staying updated lowers the risk of surprises or probate delays.

Blended families and remarriages are prevalent in Florida, making beneficiary choices complex.

Dividing assets between a current spouse, children from previous marriages, or stepchildren can be sensitive, especially if the heirs live out of state.

Florida law treats spouses differently from kids or stepkids if assets pass by default. To avoid drama, clearly spell out your wishes. If you want a charity or non-family member to inherit, double-check that their info is correct.

If any heirs reside outside of Florida, remember that state inheritance taxes and legal requirements can delay the process. For blended families, a trust helps maintain order and keep things on track.

Leaving out a contingent beneficiary can complicate things for families and estate managers. It’s especially a headache when dealing with life insurance or retirement accounts in Florida.

If the primary beneficiary can’t take the asset and there’s no contingent beneficiary named, the asset usually has to go through the Florida probate process. The court steps in and oversees who gets what.

This can drag on for months, and legal fees eat into the final payout. Families may face additional stress and lose privacy, as probate makes everything public. High-value policies and retirement accounts can be even more of a hassle.

Naming a contingent beneficiary is a quick way to dodge these headaches. Otherwise, things can get messy and expensive.

If there’s no primary or contingent beneficiary, Florida’s intestacy laws step in. That means the state’s default rules decide who gets what.

Usually, assets are distributed to close family members, such as a spouse or children. If there’s no one close, it may be passed on to distant relatives or even the state. The default rules might not match what you wanted at all.

Not naming a contingent can mean stepkids, close friends, or charities get left out—even if they mattered to you.

When there’s no contingent beneficiary, the probate court has to step in. Judges decide who inherits based on the law and whatever documents they can find.

The court might appoint a personal representative to handle the estate. They’ll:

Once the court is involved, everything slows down and gets unpredictable. Family arguments over who gets what aren’t unusual, and legal costs can pile up.

Letting a judge decide usually means you lose control over your assets. Naming contingent beneficiaries helps keep matters out of court.

Keeping your beneficiary info up to date is crucial if you want your retirement accounts, insurance, and estate documents to work the way you plan.

Life changes, and even small mistakes, can cause significant problems if you don’t act quickly.

People in Central Florida typically choose between working with an estate planning attorney or using DIY forms to update their beneficiary designations.

An attorney will review your accounts and documents, give advice, and make sure you meet legal requirements.

DIY forms are readily available, but skipping legal assistance can have unintended consequences. Online or paper forms may not adequately cover complex family setups or Florida-specific laws. Attorneys ensure that everything is in order and that loved ones aren’t left out by accident.

Review your beneficiary designations after significant life changes. Marriage, divorce, a new baby, or a death in the family often mean your old choices don’t fit anymore.

After a divorce in Florida, failing to update beneficiaries can result in assets being distributed to an ex-spouse. That’s not usually what people want.

It’s a good idea to review your designations every few years or when your financial situation changes. If you have a new child or lose a spouse, update both primary and contingent beneficiaries.

Meeting regularly with an estate planning attorney helps ensure that your wishes are clear and followed.

People often forget to list both primary and contingent beneficiaries. If your primary beneficiary can’t inherit, your assets could end up in probate or land with someone you never intended.

Always sign and submit every form carefully. I would like to request confirmation from the retirement or insurance company.

Names that don’t match between your estate documents and beneficiary forms can cause legal headaches. Keep copies of every update in a safe spot.

Let your attorney know about every change. It’s risky to rely solely on your will—here in Florida, beneficiary forms usually take precedence over the terms of the will.

Big life events happen, and people forget to update their beneficiaries. Regular reviews help you avoid accidentally leaving someone out.

Getting your estate plan in order protects your family and saves your loved ones considerable stress. When you select both primary and contingent beneficiaries, you provide clear instructions on where your assets should be distributed.

Key things to remember:

Setting up both kinds of beneficiaries keeps your wishes straightforward. It helps your family avoid confusion and sidesteps the mess of probate, ensuring assets end up with the right people.

It’s wise to review your designations during significant life events, such as marriage, divorce, or the birth of a child. Even a minor update to contact information can make a significant difference.

If you have questions or go through any life changes, reach out to a professional. Keeping your estate paperwork current now can spare your loved ones a lot of hassle down the road.

Your estate plan deserves clarity and legal strength. Let Conte Mollenhauer Law, P.A. help you secure your legacy in Florida with confidence. Schedule your personalized consultation now.

What is the difference between a primary and contingent beneficiary?

A primary beneficiary is the first person or entity named to receive assets after you pass away. A contingent beneficiary only receives assets if the primary beneficiary is unable, unwilling, or legally ineligible to inherit.

Can I name the same person as both primary and contingent beneficiary?

No, you cannot name the same individual as both primary and contingent for the same asset. A contingent beneficiary only steps in if the primary is no longer available, so the roles must be distinct.

What happens if I don’t name a contingent beneficiary in Florida?

If no contingent beneficiary is named and the primary can’t inherit, the asset may be subject to Florida probate. This can delay distribution and create legal complications for your heirs.

How many primary and contingent beneficiaries can I have?

You can name multiple primary and contingent beneficiaries for most accounts or policies. Be sure to clearly define each person’s percentage or share to avoid disputes or probate delays.

Who should I choose as my contingent beneficiary?

Choose someone you trust who can legally inherit if your primary beneficiary is unavailable. In Florida, this might be a child, sibling, trusted friend, or even a charity or trust.

Do beneficiary designations override my Florida will or trust?

Yes. Beneficiary designations on financial accounts, insurance policies, or retirement plans take precedence over the terms of your will or trust. Always keep them updated to reflect your current wishes.

Latest Post

December 16 2025

How to Open a Probate Estate in Seminole County After a Death: Forms, Steps, and Who Files What

To open a probate estate in Seminole County, families file a petition with the Seminole County...

December 16 2025

When someone passes away in Seminole County, their family often faces probate to settle the...

November 21 2025

Recording a deed in Seminole County can feel confusing. The process involves fees, paperwork, and...