Originally published: January 2026 | Reviewed by Mary Conte

In Florida, an asset usually goes through probate when it’s titled in the decedent’s name alone and lacks a built-in transfer method, such as survivorship ownership, a beneficiary designation, or trust ownership.

The fastest way to tell is to check the title, beneficiary forms, and account registration.

The difference between probate and non-probate assets depends on how ownership is structured at death.

Assets such as jointly owned property, accounts with beneficiary designations, and trust-owned property usually avoid probate entirely.

However, real estate titled in a single person’s name, individual bank accounts, and personal property without clear transfer instructions will require court oversight.

Many families discover too late that seemingly simple assets can trigger an unexpected probate case. Working with a Florida probate lawyer helps you figure out which of your assets fall into each category and plan accordingly.

One simple question determines whether an asset goes through probate in Florida: Does the asset have a named beneficiary or joint owner who automatically receives it upon death?

If the answer is no, the asset typically requires probate or another court or title transfer process to establish legal authority to retitle or release it.

When reviewing any asset, check how it is titled and whether it names someone to receive it upon death. Assets titled solely in the decedent’s name with no survivorship owner, POD/TOD beneficiary, or trust ownership are usually treated as probate assets and often require a probate case to transfer.

Assets requiring probate:

How the asset is owned determines whether probate is needed, not the asset’s type. A bank account with a payable-on-death beneficiary avoids probate.

The same account without a beneficiary is subject to probate. It’s a detail people miss all the time.

You can use this test to avoid probate by adding beneficiaries or joint owners to your assets. This is the foundation of probate avoidance planning in Florida.

Mary Conte Law can map your assets into probate or non-probate on a single call, so your family avoids delays later. Schedule an appointment.

If you’re ready to get started, call us now!

How property is titled determines whether it goes through probate or transfers directly to the survivors. Florida homestead property receives special protections, but often still requires court involvement even when it avoids full probate.

When you own Florida real property in your name alone, it must go through probate. A deed that lists “John Smith” as the sole owner requires court proceedings to transfer the property to the heirs or beneficiaries.

Tenants in common ownership also triggers probate for your share. If two people own property as tenants in common and one dies, that person’s share passes through probate rather than automatically to the surviving owner.

Joint ownership with right of survivorship allows property to transfer automatically outside of probate. The deed must include specific survivorship language such as “joint tenants with right of survivorship” or “husband and wife.”

Without this exact wording, the property defaults to a tenancy-in-common ownership. It’s a technicality, but it matters a lot.

An enhanced life estate deed, commonly called a ladybird deed, lets you retain full control during your lifetime while naming beneficiaries who receive the property automatically at death.

This avoids probate entirely while allowing you to sell or mortgage the property without beneficiary approval. Not everyone knows about this option, but it can be a lifesaver.

Florida homestead protections don’t automatically eliminate court filings. Families often still need a probate court determination (or related filings) to confirm homestead status and establish insurable title for transfers or refinancing.

Florida restricts who can receive a homestead by will when there’s a surviving spouse or minor child; a homestead generally is not subject to devise in those situations, except it may be devised to the spouse if there is no minor child.

If devise restrictions apply, how the spouse and descendants take homestead is governed by Florida law (including the spouse’s life estate/tenant-in-common election framework), and the paperwork is often required to obtain a clean title.

If you have minor children, they may have ownership rights that require court supervision.

Even when your homestead is protected from creditors and passes to family automatically by law, your personal representative must file documents with the probate court.

These filings confirm the property’s homestead status and identify the rightful heirs. Without this court paperwork, title companies typically won’t insure the property for sale or refinancing.

How bank accounts are titled determines whether they go through probate in Florida. Accounts with proper beneficiary designations or joint ownership typically avoid probate, while sole-name accounts must go through the court process.

Payable-on-death (POD) accounts generally transfer to the named beneficiary by operation of law under Florida’s POD account statute, outside probate. When you set up a POD designation, the money in your checking or savings account transfers to the person you choose immediately upon your death.

The assets are bypassed entirely by the court process. Your beneficiary simply needs to present a death certificate to the bank to claim the funds.

Bank accounts with POD or beneficiary designations do not go through probate court. This includes checking, savings, and certificate of deposit accounts with these designations.

If there’s no POD beneficiary (or the designation fails), the account is typically treated as a probate asset and often requires estate administration to release/retitle. It’s an easy thing to overlook, but it makes a big difference.

Joint accounts with rights of survivorship automatically pass to the surviving account holder upon the death of one owner. The account must specifically include survivorship language to avoid probate.

Joint tenants with rights of survivorship means the surviving owner receives full control of the account. The funds do not become part of your probate estate.

Some people add another person to their account for convenience only. These “convenience” accounts may create problems if the joint owner wasn’t meant to inherit the money.

Whether probate is needed depends on how the account was set up and whether it includes the right of survivorship. Jointly owned property in bank accounts needs clear documentation showing survivorship intent.

If you’re ready to get started, call us now!

Brokerage accounts holding stocks, bonds, and mutual funds typically go through probate unless you designate beneficiaries.

Florida law allows you to name transfer-on-death beneficiaries on investment accounts to avoid the probate process entirely.

Florida permits TOD registration in beneficiary form for securities under Chapter 711, allowing qualifying accounts to pass to beneficiaries outside probate when properly registered.

When you add a TOD beneficiary to your account, the assets pass directly to that person after your death without court involvement.

You can set up TOD registrations for individual stocks, bonds, mutual funds, and exchange-traded funds held in your brokerage account.

The process involves completing paperwork with your financial institution to name one or more beneficiaries.

What happens without a TOD designation:

Your beneficiaries need to provide a death certificate and identification to claim the assets. You can change or remove TOD beneficiaries at any time while you are alive.

The designation only takes effect after your death, so you maintain full control of your investments during your lifetime.

If all named beneficiaries die before you and you do not update the designation, the assets revert to your estate and go through probate.

Life insurance policies and retirement accounts avoid probate when you name beneficiaries directly on these accounts. The funds go directly to the people you listed, bypassing the court system entirely.

Your primary beneficiary is the first in line to receive your account upon your death. The contingent beneficiary receives the funds if your primary beneficiary dies before you or is unable to take them.

Assets with designated beneficiaries bypass probate entirely because the bank or company pays them directly to your chosen people. This covers 401(k)s, IRAs, life insurance, and annuities.

The biggest headache? Forgetting to name any beneficiaries at all. Retirement accounts go through probate if you don’t pick a valid beneficiary before you pass.

This same mess pops up if all your beneficiaries die before you update the paperwork. Your account then becomes part of your probate estate because no one is designated to receive it.

Common beneficiary designation mistakes that trigger probate:

It’s smart to check your beneficiary designations every few years. Life happens—marriage, divorce, kids, and deaths mean you should update these forms to keep your accounts away from probate court.

Whether a vehicle or boat requires probate depends on its title status and value. Items with certificates of title follow different rules from things like jewelry or household goods.

Titled personal property includes vehicles, boats, motor homes, and big trucks that need a certificate of title to prove ownership.

A titled vehicle may require probate, but Florida also allows certain DHSMV/statutory title transfers by operation of law, depending on the facts (e.g., spouse/heir scenarios), and joint titling or trust ownership can avoid probate.

Disposition without administration is not a ‘<$75,000’ rule. It applies only when the estate consists of exempt property plus nonexempt personal property not exceeding preferred funeral expenses and last-60-days medical/hospital expenses.

The key difference: If an item has a state-issued title, you’ll need to follow legal procedures to transfer ownership. If there’s no title, your stuff can usually pass to heirs with less hassle.

Whether a vehicle needs probate depends on the title/ownership and whether the facts qualify for a statutory/DHSMV transfer process; avoid assuming ‘exempt vs non-exempt’ is the deciding test. Joint ownership, transfer-on-death designations, and living trusts can help you avoid probate for titled items.

A revocable living trust only keeps assets out of probate if you actually move those assets into the trust’s name. Just making the trust document isn’t enough.

When you create a trust, you sign legal documents that set out how your assets will be managed. You end up with a trust agreement on paper, but your property doesn’t change hands yet.

Funding the trust means you retitle your assets in the trust’s name. You must update the bank accounts, real estate deeds, and investment accounts so the trust owns them.

A trust only avoids probate for assets it officially owns. If you don’t fund your trust, your assets still go through probate when you die because they’re still in your name. Your successor trustee can’t hand out unfunded assets directly to your beneficiaries.

Lots of families find this out the hard way after a loved one passes. They discover a signed trust but realize the person never moved their home, car, or bank accounts into it.

A properly funded revocable living trust avoids probate, but an unfunded trust doesn’t protect anything.

Unsure whether your home, accounts, or vehicle will transfer automatically? A quick review with Mary Conte Law can clarify. Contact us.

If you’re ready to get started, call us now!

Some assets just slip through the cracks during estate planning. They seem minor or don’t feel like “real” property, but they can still force your family into probate court, dragging things out and costing thousands.

Your ownership stake in a business or LLC goes into your probate estate if you haven’t set up a transfer plan.

Tons of business owners are so busy running their businesses that they forget to include ownership interests in their estate plans.

Business interests are often drawn into estate administration unless they’re held in a trust or governed by enforceable buy-sell succession terms; even then, transfers may still require formal documentation and authority.

Even a tiny ownership interest in a local business can go through probate without a beneficiary or transfer mechanism.

This gets worse when there are multiple owners. Your death can throw business partners into probate court instead of letting them just run the company.

Setting up an LLC operating agreement with succession provisions can save everyone a headache.

Your cryptocurrency wallets, online investment accounts, and digital businesses have real value and become part of your probate estate.

Families sometimes find these hidden estate assets after digging through emails or random statements.

Digital assets may require probate authority (or other legal authorization) to access and transfer them—especially if login credentials, proof of ownership, or platform procedures aren’t documented. Florida courts require proof of ownership before releasing these assets to heirs.

The real challenge with digital property? Families might not even know these accounts exist.

You should make a secure list of all your digital assets, including login info, and stash it somewhere your executor can find it. Otherwise, valuable accounts might just stay forgotten during the probate process.

Timeshare interests often trigger probate or title-transfer paperwork when deeded/titled solely in the decedent’s name; the key is how the interest is titled and recorded. Many people think timeshares aren’t significant, but the title still has to go through probate.

Collectibles like coin collections, old cars, or art become probate assets if they have certificates of authenticity or official titles. A classic car titled in your name alone triggers probate, even if it’s not worth much.

Small bank accounts at credit unions or local banks are easy to forget in estate planning.

If you opened an account years ago and left it inactive, that $800 still requires probate. Safety deposit boxes create similar headaches—the contents have to be inventoried and distributed through your probate estate.

Boats, RVs, and motorcycles titled solely in the decedent’s name may require probate or a statutory transfer process; joint survivorship titling or trust ownership are common ways to reduce probate exposure.

Even if you’ve set up most assets to bypass probate, your family might still need to open a probate case for legal or administrative reasons. Summary administration and ancillary probate can pop up despite your best planning.

Probate should clear up title issues, even if the estate’s value is small. Banks, title companies, and buyers sometimes refuse to transfer assets without a court order, especially with old accounts or real estate with messy records.

Common situations requiring probate filing:

Your estate might qualify for summary administration in Florida if the total value is under $75,000 or the person died more than 2 years ago. This process is faster and less expensive than formal probate.

Creditor claims can also force probate, even when all assets are set up as non-probate. You’ll need the court to resolve debts and protect your beneficiaries from future issues.

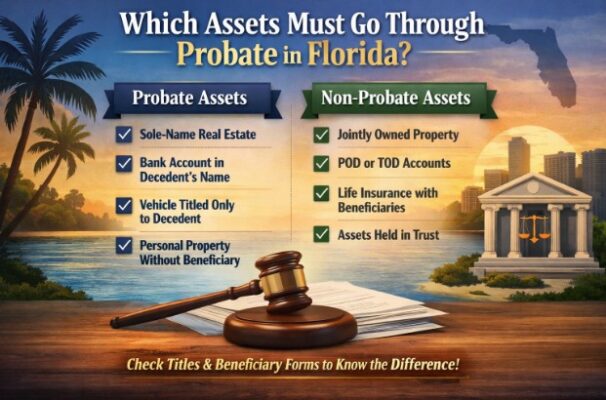

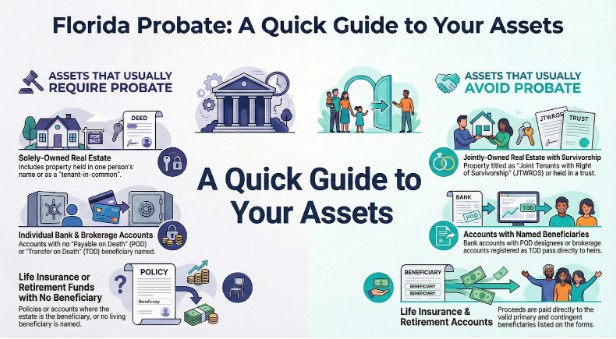

When someone dies in Florida, it’s important to know which assets require court administration and which pass directly to beneficiaries.

The difference between probate and non-probate assets mostly depends on how each asset is titled and whether there’s a beneficiary named.

Probate Assets are assets owned solely in the deceased person’s name and do not have an automatic transfer mechanism. These assets must go through the court process before anyone can distribute them.

Non-probate assets skip probate entirely. These assets that pass directly to survivors include property with beneficiary designations or joint ownership setups.

| Asset type | Usually probate? | Usually non-probate? | The fastest thing to check |

| Florida real estate | Sole-name deed; tenant-in-common share | JTWROS/TBE survivorship deed; trust-owned; enhanced life estate (“Lady Bird”) deed | Deed wording + how owners are listed |

| Bank accounts | Sole-name w/ no POD | POD/ITF accounts; joint accounts with survivorship | Bank signature card + beneficiary form on file |

| Brokerage/securities | No TOD registration | TOD-registered securities | Beneficiary/TOD registration status |

| Life insurance/annuities | Payable to the estate or no living beneficiary | Named primary + contingent beneficiary | Beneficiary designations (primary/contingent) |

| Retirement (401k/IRA) | Failed/missing beneficiaries | Valid beneficiary designations | Beneficiary forms updated after life events |

| Vehicles/boats (titled) | Sometimes, depending on the title + facts | Joint survivorship title; trust-owned; may qualify for DHSMV/statutory transfer process | Title + whether spouse/heirs can use §319.28/DHSMV procedure |

| Exempt property | Still needs the correct procedure | May be handled via a limited court process or disposition without administration (only in narrow cases) | Whether the estate is only exempt property + final expenses |

Knowing which category your assets fall into helps as you plan your estate. If you’re dealing with assets subject to probate in Florida, you’ll face formal court proceedings.

Non-probate assets, on the other hand, transfer automatically upon death. Simple as that, but it’s always wise to double-check your own situation.

Turn this checklist into a real plan—update beneficiary information, confirm the deed wording, and fund your trust. Schedule an appointment with Mary Conte Law.

Which assets must go through probate in Florida?

Assets typically require probate when they’re owned in the decedent’s individual name with no survivorship co-owner, no beneficiary designation, and not titled in a trust—such as sole-name real estate or a sole-name bank account without POD.

Do jointly owned assets avoid probate in Florida?

Often, yes. Assets held as “tenancy by the entireties” (for many married couples) or “joint tenants with right of survivorship” usually transfer automatically to the surviving owner and do not pass through probate.

Do payable-on-death (POD/ITF) bank accounts go through probate in Florida?

No, not when the POD/ITF designation is properly set up, and the beneficiary is alive. Florida law treats POD accounts as transfers that occur by account contract at death, outside probate administration.

Do transfer-on-death (TOD) brokerage accounts avoid probate in Florida?

Usually, yes. Florida’s TOD security registration rules allow securities registered in beneficiary form to transfer at death by contract with the financial institution, which is treated as non-testamentary and generally avoids probate.

Does Florida homestead still require probate paperwork?

Sometimes. Florida homestead has protections and special rules, but there are devise restrictions when a spouse or minor child survives. Families often still need court filings to confirm status and establish a clean, insurable title.

What happens if a beneficiary designation is missing or outdated?

If an account has no valid living beneficiary—or the designation fails—the asset can revert to the estate and become subject to probate. This is common with retirement accounts or insurance when forms weren’t updated after life changes.

Do trusts avoid probate automatically in Florida?

Only for assets the trust actually owns. A revocable trust can help avoid probate, but if accounts and deeds were never retitled into the trust (unfunded trust), those assets may still require probate.

Latest Post

January 14 2026

What Is Florida Probate and When Is It Required? A Plain-English Guide for Families

When someone dies in Florida, their family often faces an unfamiliar legal process called...

January 14 2026

Florida probate is the court-supervised process that authorizes a personal representative to...

January 14 2026

Which Assets Must Go Through Probate in Florida (And Which Do Not)?

In Florida, an asset usually goes through probate when it’s titled in the decedent’s name...