Millions of Florida homeowners wonder what happens to their mortgage when they move their house into a trust, especially those focused on protecting their assets and streamlining their estate plans.

Putting a house with a mortgage into a trust in Florida does not require paying off the loan or trigger the mortgage’s due-on-sale clause.

This means owners can generally move their property into a revocable living trust without worry.

This helps ensure the home is managed as part of their larger estate plan.

While transferring a mortgaged home into a trust may sound complicated, the daily responsibilities, such as paying your mortgage and property taxes, usually remain unchanged for the homeowner.

It’s important to watch out for possible tax impacts or mistakes that could affect your homestead exemption.

Some legal paperwork and potential costs, such as documentary stamp taxes, may apply depending on the specific situation.

Transferring a house with a mortgage into a Florida trust involves important legal protections and specific rules.

Homeowners should be aware of how federal law interacts with lender agreements to help avoid unexpected challenges.

A due-on-sale clause is a common part of most mortgage agreements.

It gives the lender the right to demand full payment of the mortgage if the property is transferred to someone else without approval.

In Florida, many people worry that transferring a home to a living trust may trigger this clause.

If a lender enforces the due-on-sale Florida trust rule, the homeowner may be required to pay the remaining balance immediately.

While some lenders may agree to the transfer, it is essential to check the mortgage paperwork and contact the lender before beginning the process.

Here are the main points about the due-on-sale clause:

The Garn-St. The Germain Depository Institutions Act provides key protection for individuals who wish to place mortgaged homes into a revocable living trust.

This federal law prevents lenders from enforcing the due-on-sale clause when a homeowner transfers the property into a trust, as long as the person remains a beneficiary and the trust is established for estate planning purposes.

This means most Florida homeowners can move property into a living trust without needing to pay off the mortgage first.

The act specifically protects family homes used for personal occupancy, not investment properties.

Key facts about the act:

Worried your mortgage might complicate your trust? Conte Mollenhauer Law assists Florida homeowners in structuring revocable trusts without triggering lender issues. Contact us to secure your estate plan today.

If you’re ready to get started, call us now!

Transferring a Florida homestead into a trust changes the property’s title, but does not erase or forgive the mortgage attached to the home.

Homeowners should be aware of how this affects their mortgage, lender rights, and future refinancing or borrowing options.

When an owner places a mortgaged home into a trust in Florida, the property title changes, but the mortgage obligation remains with the borrower.

The lender’s lien on the property remains in effect, regardless of whether the ownership is in an individual’s name or the name of a trust.

This transfer does not pay off the bank.

The homeowner must continue making payments as before.

The actual mortgage liability after a trust transfer in Florida remains unchanged unless the borrower refinances or pays off the loan.

Lenders may require notice of the transfer to the trust.

The trust document and deed must be prepared carefully to keep homestead protections intact.

Guidance from a qualified attorney is recommended, especially when handling a mortgage when a house is in trust in Florida.

Many homeowners worry that moving a mortgaged home into a trust will trigger a lender’s “due-on-sale” or acceleration clause.

However, under federal law, specifically the Garn-St..Under the Germain Act, an owner can transfer a primary residence into a revocable living trust without the lender calling the full loan due.

The key is that the trust must be revocable, and the borrower must remain a beneficiary who uses the home as their primary residence.

If these conditions are met, the lender cannot accelerate the mortgage simply because the title changed.

Problems can arise if the trust is irrevocable or doesn’t allow the borrower to live in the home.

Refinancing after placing a home in a trust is possible, but some lenders may require the property to be retitled back to the owner’s name before approving a new loan.

Once the new mortgage is in place, the property can usually be transferred back into the trust.

Second mortgages follow similar rules.

Lenders look closely at trust terms and beneficiaries before allowing a second lien.

They want to ensure that their lien priority and foreclosure rights are protected in the event of a default.

For those considering a second mortgage on a trust property in Florida, clear communication with the lender and a thorough legal review of the trust are crucial steps to avoid delays and protect your legal rights.

When a Florida homeowner transfers property into a trust, it can affect property taxes, documentary stamp taxes, and legal protections.

Planning and the way the trust is written are crucial for maintaining homestead benefits and avoiding additional costs or risks.

A homeowner in Florida can keep the homestead exemption even if a trust owns the home.

The key is that the trust must give the homeowner a present possessory interest—the legal right to live in the home for the remainder of their life.

If the trust is set up correctly, the property can still qualify for the Florida homestead tax exemption.

This helps homeowners maintain lower property taxes and benefit from the “Save Our Homes” cap, which limits yearly tax increases.

For example, under section 196.041(2) of the Florida Statutes, the resident beneficiary must have the right to use and live in the property.

Mistakes in the trust documents may result in loss of the exemption or higher taxes, so legal review is important.

If the exemption is lost, property taxes can go up sharply.

Transferring a home into a trust in Florida does not always result in additional documentary stamp taxes.

Most of the time, if the person creating the trust (the grantor) remains the main beneficiary and there is no change in the mortgage, no additional stamp tax is due.

However, things change if there is a mortgage on the property.

If the trust agreement alters who is responsible for the mortgage or if the lender retitles the mortgage to the trust, Florida law may treat this as a new transaction.

This can result in extra documentary stamp taxes, sometimes based on the unpaid balance of the mortgage.

Homeowners in Florida should consult professionals about documentary stamp taxes on trusts and mortgages to avoid unexpected costs.

Different rules may apply if the trust names new beneficiaries other than the original owner or spouse.

Seeking legal advice is advisable to avoid tax complications.

Florida provides strong homestead protections, even if the property is in a properly drafted trust.

The Florida constitution protects the primary home from most creditors and forced sale, as long as the person who set up the trust (the settlor) has the right to live in the house.

If the trust limits this right or says the house must be sold after death, those protections can be weakened or lost.

This means the setup of the trust is critical.

More information about keeping Florida trust title homestead protection is available for those considering this move.

Homestead properties in trust are not immune from foreclosure for missed mortgage payments or unpaid property taxes.

These debts can still result in the loss of the property if not addressed promptly.

When placing a home with a mortgage in a trust in Florida, misunderstandings about payments, homestead protections, and mortgage clauses can lead to mistakes that result in legal or financial trouble.

Paying close attention to these details helps homeowners avoid headaches that may arise after the transfer.

Some people believe that once the deed is moved into a trust, they are no longer responsible for their loan.

This is incorrect.

The borrower named on the mortgage remains fully responsible for making all mortgage payments, no matter who owns the deed.

If payments stop, the lender can foreclose, even if the house is in a trust.

The mortgage does not disappear or change just because the title transfers.

Transferring the deed is not the same as paying off or refinancing the loan.

Trust documents usually do not change the terms of any mortgage agreement.

Homeowners should notify their lender and make sure payments remain up to date after the transfer.

In Florida, the homestead exemption offers important property tax and creditor protections. Many think they will lose these benefits by titling their home in a trust.

Normally, this is not the case if the trust is set up correctly. If the person living in the home is also a trust beneficiary and the trust allows them to use the property as their primary residence, Florida law permits the homestead status to remain.

It’s essential for a trust agreement to include language that demonstrates the owner’s right to reside in the home. Failing to follow these requirements, however, can result in the county revoking the exemption.

This could lead to higher taxes or loss of creditor protection. Legal review during setup is crucial to maintain these benefits.

A common concern is that the lender will activate the “due-on-sale” clause when a house is placed into a trust. The due-on-sale clause is a provision in a mortgage that allows the lender to demand payment in full if the property changes ownership.

However, under federal law, especially the Garn-St.. The Germain Depository Institutions Act states that banks cannot enforce this clause simply because a homeowner transfers their primary residence into a revocable trust, as long as the borrower is a trust beneficiary and continues to reside in the property.

This protection applies in Florida, meaning that simply placing a home in a revocable living trust should not trigger a due-on-sale clause in a mortgage. If the trust is irrevocable or set up differently, risks may appear, so it is smart to consult with the lender.

A misstep in retitling a mortgaged home can cost you thousands of dollars. Conte Mollenhauer Law handles trust deed transfers the right way—start-to-finish clarity. Reach out now to schedule your trust consultation.

If you’re ready to get started, call us now!

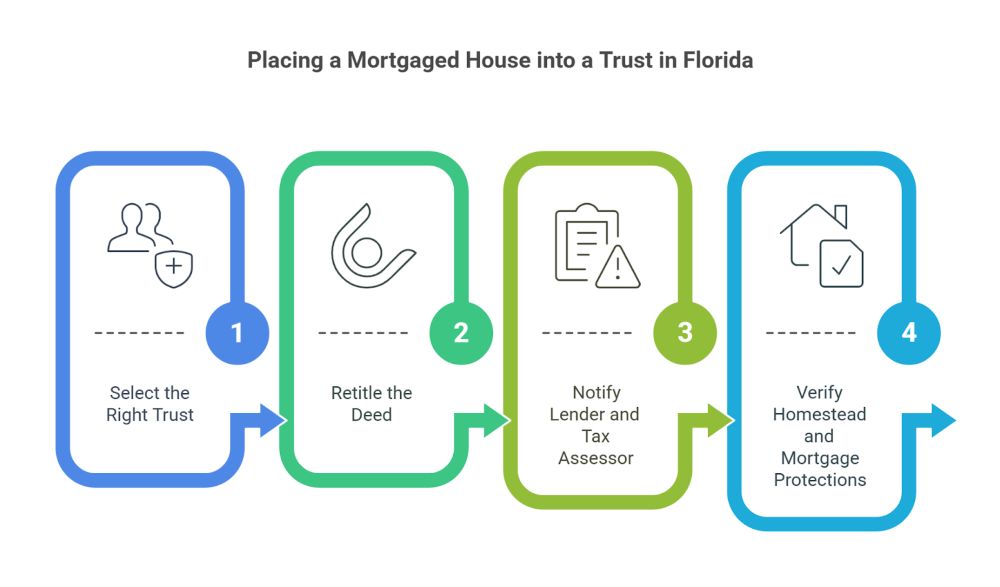

In Florida, placing a house with a mortgage into a trust involves updating legal documents, considering lender policies, and ensuring protections such as the homestead exemption remain in place.

Each step requires care to prevent issues with ownership, taxes, or the mortgage.

Choosing between a revocable living trust and an irrevocable trust affects control and flexibility. A revocable trust allows the homeowner to change or terminate the trust at any time, making it easy to manage and modify as life changes.

This type is usually favored when a mortgage is present because it remains in the owner’s control. An irrevocable trust means relinquishing control over the property.

Changes require approval from everyone named in the trust. This option provides stronger asset protection but can trigger lender due-on-sale clauses, which may prompt the bank to demand immediate payment of the full loan balance.

Most people with a mortgage in Florida use a revocable trust to avoid complications.

Transferring a home into a trust means updating the deed to show the trust as the new legal owner. In Florida, a new deed—most often a quitclaim or warranty deed—is prepared and signed, transferring the property from personal ownership to the trust.

This step is required to make the trust valid in the official property records. The signed deed must be recorded with the county clerk or recorder’s office in the county where the property is located.

Failure to record the deed can lead to confusion or disputes later about who owns the home. Some counties may charge fees or taxes, like documentary stamp taxes, especially if the house has a mortgage.

Following the correct recording process is crucial to ensuring the property is properly transferred into the trust.

Although not always required, contacting your mortgage lender is generally advisable when placing a house in a trust. The mortgage agreement may include a “due-on-sale” clause.

This clause sometimes allows the lender to request the full balance if the deed is changed. Most lenders, however, do not enforce the clause for revocable trusts where the owner is still the borrower.

Still, it is safest to inform the lender and get written approval or confirmation that the trust transfer will not cause any problems. The county tax assessor should also be notified so the property records are up to date.

This can help prevent mistakes with your tax bills or the application of homestead exemptions. It may also expedite the process if questions about ownership or taxes arise later.

Staying transparent with both the lender and the tax assessor lowers future risk.

Florida’s homestead laws provide significant protections, including reduced property taxes and exemption from certain creditors.

When transferring a mortgaged home into a trust, it is crucial to verify that the homestead exemption is not forfeited, as errors in paperwork or titling can render these benefits invalid.

For married couples, careful attention should be given to how the property is titled within the trust to ensure both partners retain their rights.

Similarly, homeowners should check that mortgage protections, such as foreclosure procedures and notification rights, continue unchanged after the transfer.

Regularly reviewing these protections with a legal or estate planning professional can help prevent problems and ensure important rights remain intact.

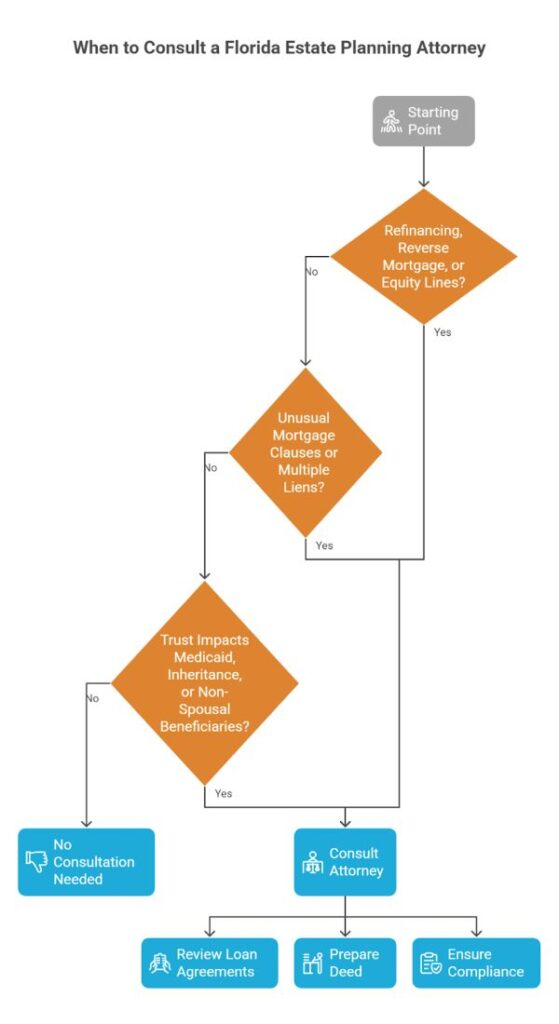

Certain situations create legal and financial risks when transferring a mortgaged home into a trust. These may involve lender requirements, unique mortgage clauses, Medicaid planning, or complex inheritance goals.

Transferring a home into a trust can create complications when dealing with lenders or changing loan terms. Before starting a refinance, applying for a reverse mortgage, or adding a home equity line of credit, it is critical to involve an attorney.

Banks often require the home to be retitled in the owner’s name before approving these loans. A reverse mortgage and trust in Florida present unique rules and regulations.

Lenders may not allow this type of mortgage to remain or be originated if certain trusts hold the property.

An attorney can help identify these restrictions and minimize disruption to securing or keeping these loans.

Common tasks a lawyer can help with include:

Some mortgages in Florida have “due-on-sale” or acceleration clauses. This means the loan could become due immediately if ownership changes, even if the property is transferred into a trust.

If the property has multiple liens, such as second mortgages or unpaid contractor bills, trust transfers can get complicated. Every lienholder’s consent might be needed, and missing a step can result in loan default or even foreclosure.

A Florida estate attorney reviews all liens and mortgage documents before any transfer. They communicate with lienholders, get written approvals when necessary, and prevent costly mistakes.

In situations with multiple loans or unique loan terms, their advice helps avoid unwanted legal trouble.

Transferring property to a trust affects eligibility for government benefits, inheritance rights, and property rights of non-spouses.

For example, Medicaid planning involves strict asset transfers and look-back periods.

Errors in trust setup could disqualify a homeowner from Medicaid coverage for nursing care.

Naming non-spouse heirs—like children or siblings—as trust beneficiaries adds extra legal steps.

An estate lawyer ensures that all transfer paperwork complies with Florida law, which is crucial for both Medicaid eligibility and inheritance planning.

A professional can also help avoid gift tax issues or unintended loss of homestead protection.

Don’t risk losing your homestead benefits or upsetting your lender. Conte Mollenhauer Law ensures your trust protects both your property and your peace of mind. Contact us today to get your plan underway.

Does my mortgage transfer to the trust when I retitle my home?

No, your mortgage stays in your name. The trust holds legal title, but you remain responsible for the loan. Payments and lender obligations don’t change after transfer.

Will my lender call the mortgage due if I put my house in a trust?

No, not if you’re using a revocable living trust. Under the Garn-St. The Germain Act (12 U.S.C. § 1701j-3) prohibits lenders from enforcing a due-on-sale clause in this situation.

Can I refinance my home after placing it in a trust?

Yes, but your lender may require you to retitle the home in your name temporarily. After refinancing, you can transfer the property back into the trust.

Does transferring a mortgaged property into a trust trigger any tax implications?

It may. Florida documentary stamp taxes can apply if the trust assumes or is tied to mortgage debt. An attorney can help determine if an exemption applies.

Will putting my house in a trust affect my homestead exemption in Florida?

No, as long as the trust is properly structured. You must retain a beneficial interest and reside in the property to keep Florida’s homestead tax benefits.

Can I transfer a home with a reverse mortgage into a trust?

It depends on your lender and the type of trust. Many reverse mortgages don’t allow transfers without lender approval, especially if using an irrevocable trust.

Latest Post

September 19 2025

Seminole County Probate: Summary vs. Formal (Eligibility, Steps, Fees)

When someone passes away in Seminole County, Florida, their estate usually lands in probate...

September 19 2025

In Seminole County, Florida, some small estates qualify for the disposition of personal property...

September 19 2025

Seminole Probate Packets & Where to File Addresses, Hours, e-Filing, and e-Recording Guide

Filing probate in Seminole County involves determining which packets are required and where to...