Originally published: June 2025 | Reviewed by Mary Conte

Starting a holding company in Florida can be a smart strategy for protecting your assets and organizing multiple businesses under one umbrella.

A Florida holding company offers significant tax advantages, liability protection, and simplified management of diverse business interests.

Many entrepreneurs and investors choose Florida for its business-friendly environment and lack of state income tax, making it an attractive location compared to other popular states like Wyoming, Delaware, or New Mexico.

Setting up your holding company involves several straightforward steps, from selecting the right business structure (typically an LLC) to registering with the state and establishing proper financial controls.

While the process might seem complex at first, breaking it down into manageable steps makes it accessible even for those new to holding company structures.

A holding company is a business entity that doesn’t conduct operations itself but exists to own assets such as stocks, real estate, trademarks, and subsidiaries.

Its primary purpose is to control other companies by owning their voting stock while protecting valuable assets.

Think of it as a parent company that oversees and manages its children’s companies. The main benefits include:

Holding companies don’t typically produce goods or services themselves. Instead, they focus on owning and controlling assets while the subsidiaries handle day-to-day operations.

Florida has become a popular destination for setting up holding companies due to its business-friendly environment. The state offers several compelling advantages:

No state income tax: Florida residents and businesses avoid state income taxes, creating significant savings compared to high-tax states.

Strong asset protection laws: Florida provides robust protection for business assets, including specific statutes that shield company owners.

Privacy protection: The state offers good privacy options for business owners who prefer discretion regarding their holdings.

The warm climate and high quality of life also attract business owners who want to establish residency where their holding company operates.

Florida’s growing economy and business infrastructure provide additional support for various types of business ventures.

Entrepreneurs can establish several types of holding companies in Florida, each with distinct characteristics and benefits:

Pure Holding Company: This entity exists solely to own shares of other companies without conducting any operations itself.

Mixed Holding Company: Owns subsidiaries but also engages in its own business activities, providing services or producing goods.

Intermediate Holding Company: Operates between a parent company and subsidiaries, often used in complex corporate structures.

Most Florida holding companies are structured as one of these legal entities:

The LLC structure is particularly popular for Florida holding companies because it combines liability protection, operational flexibility, and favorable tax treatment.

Selecting the appropriate legal structure is the foundation of your Florida holding company. This decision will impact your liability protection, tax obligations, and how you manage your business assets.

When establishing a holding company in Florida, you’ll primarily choose between an LLC (Limited Liability Company) or a corporation. Both structures offer distinct advantages.

Limited Liability Company (LLC)

Corporation

Most Florida holding companies choose the LLC structure for its flexibility and tax benefits. LLCs are particularly advantageous for real estate holdings and family businesses.

The structure you select carries significant legal and tax consequences that will affect your holding company’s operations.

Tax Considerations:

Legal Protections:

Florida offers tax advantages for holding companies, with no state income tax on either structure. This makes Florida particularly attractive compared to other states for establishing a holding structure.

Ownership arrangements differ significantly between LLCs and corporations, affecting the control and management of your assets.

In an LLC, owners (called members) hold membership interests rather than stock. Members can establish a customized operating agreement that defines ownership percentages, voting rights, and profit distribution.

This flexibility allows for creative ownership structures tailored to your specific needs.

Corporations issue stock to shareholders, who then elect a board of directors. This creates a more rigid ownership hierarchy but provides clear governance for larger or more complex holdings. Corporations can also create different classes of stock with varying rights.

For family-based holding companies, LLCs often provide better options for succession planning and asset protection. They allow for easier transfer of ownership interests while maintaining control within the family.

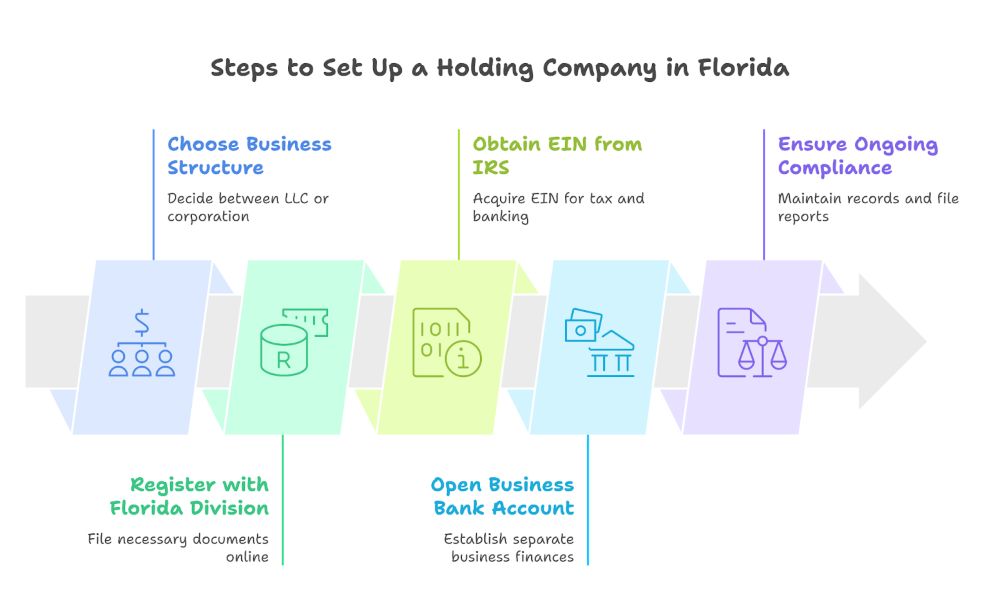

Registering your holding company with the State of Florida requires several critical steps. These include selecting a unique business name, filing the appropriate formation documents, designating a registered agent, and obtaining the necessary tax identification.

Before registering your Florida holding company, select a unique business name that complies with state regulations.

Depending on your chosen structure, the name must include a business identifier such as “LLC,” “Inc.,” or “Corporation.”

To check name availability, conduct a business name search through Florida’s Division of Corporations database (Sunbiz). This step prevents you from selecting a name already in use.

Florida requires your business name to be distinguishable from other registered entities. Consider these naming requirements:

For a small fee, you can reserve your chosen name for up to 120 days by filing a name reservation application with the Florida Department of State.

The core registration document for your holding company depends on your business structure. You’ll need to file Articles of Organization for an LLC, while corporations require Articles of Incorporation.

These documents can be submitted online through the Florida Department of State’s Sunbiz website or by mail. The filing fee for an LLC is $125, and corporations typically cost $70 plus a designation fee.

Your filing must include:

For LLCs:

For Corporations:

Processing typically takes 7-10 business days, though expedited options are available for an additional fee.

Florida law requires your holding company to maintain a registered agent within the state. This agent receives legal documents and official correspondence on behalf of your business.

Your registered agent must:

You can serve as your own registered agent if you maintain a physical presence in Florida. However, many holding companies choose professional registered agent services to ensure compliance and privacy.

Your formation documents must include the agent’s information. Changing your registered agent later requires filing a Change of Registered Agent form with the state.

After state registration, your holding company needs an Employer Identification Number (EIN) from the Internal Revenue Service. Think of this as your business’s social security number for tax purposes.

You can apply for an EIN:

The EIN is essential for:

The application is free, and online applications receive an EIN immediately. Keep this number in your permanent business records, as you’ll need it for all future tax and banking activities.

Worried about legal risks, tax complications, or losing control over your assets? A well-structured holding company can safeguard your business and wealth. Mary Conte Law ensures everything is set up correctly—schedule your consultation today!

If you’re ready to get started, call us now!

After forming your Florida holding company, you must set up proper infrastructure to manage assets, track financials, and establish operational guidelines. These elements create the foundation for efficient asset management and legal protection.

Opening a separate bank account for your holding company is essential for maintaining the corporate veil. This separation protects personal assets from business liabilities.

When selecting a bank, consider these factors:

Required documents typically include:

Banking separation creates clear financial boundaries between the holding company and subsidiary businesses. It also simplifies tax preparation and financial reporting at year-end.

Accurate financial tracking is crucial for a holding company’s effectiveness. Implementing proper accounting systems helps monitor asset performance and ensures compliance with tax regulations.

Essential accounting practices include:

Florida holding companies face specific tax considerations, including:

Consider hiring a CPA with holding company experience to ensure proper reporting of intercompany transactions and dividend distributions. Regular financial reviews help identify potential tax savings opportunities.

Operating agreements (for LLCs) or corporate bylaws (for corporations) establish your holding company’s governance structure and operational rules. These documents are not publicly filed but serve as internal guidelines.

Key elements to include:

These documents should address state requirements for Florida holding companies regarding annual reports and registered agent maintenance.

The agreement should also detail how assets will be managed between the holding company and operating subsidiaries. This includes loan terms, lease agreements, and intellectual property licensing arrangements.

Well-drafted governance documents protect owners during disputes and clarify operational procedures when managing multiple assets.

Setting up a holding company in Florida involves several tax and compliance obligations that require careful attention.

Understanding these requirements will help you maintain good standing and maximize the tax benefits available to your structure.

Florida holding companies enjoy significant tax advantages compared to many other states.

Most notably, Florida does not impose a personal income tax, which can create favorable conditions for business owners. For federal taxes, the structure of your holding company determines its tax treatment.

LLCs typically enjoy pass-through taxation, meaning profits flow directly to owners’ personal tax returns. C-Corporations face potential double taxation on profits and dividends, while S-Corporations may offer tax savings on self-employment taxes.

Florida does impose a corporate income tax (currently 5.5%) on C-Corporations, but properly structured holding companies can often minimize this burden through careful planning.

Many holding companies utilize strategies like proper expense allocation between entities to optimize their tax position.

Key Florida Tax Benefits:

Every Florida holding company must file an annual report with the Florida Department of State by May 1 each year. This filing maintains your company’s active status and keeps your business information current in state records.

The annual report filing fee is $138.75 for LLCs and $150 for corporations. Failure to file on time results in a $400 late fee and could eventually lead to the administrative dissolution of your company.

Beyond annual reports, maintaining proper corporate records is essential. This includes keeping meeting minutes, tracking resolutions, and maintaining separate financial accounts for each entity in your holding structure.

Regular reviews of your registered agent information ensure you’ll receive important legal and tax notices. Many holding companies designate a professional registered agent service to fulfill this requirement.

Depending on their activities, holding companies in Florida may be subject to various transactional taxes. If your holding company sells tangible goods retail, it must register with the Florida Department of Revenue and collect sales tax (currently 6% plus local surtaxes).

Payroll tax compliance is mandatory for holding companies with employees. This includes federal employment taxes (Social Security, Medicare, federal unemployment) and state-specific requirements, such as the Florida reemployment tax.

Many pure holding companies have minimal sales tax exposure since they primarily hold assets rather than conduct active business operations. However, subsidiary operating companies will likely face these obligations.

Florida holding companies offer powerful legal structures that can significantly protect your personal and business assets from creditors and lawsuits. Proper planning creates multiple layers of protection while maintaining operational efficiency.

Holding companies act as a protective shield for valuable assets by keeping them separate from operational risks.

In Florida, LLC asset protection occurs when you structure a limited liability company specifically to protect ownership interests from business liabilities.

The key advantage is the “charging order protection” provided by Florida law. This protection prevents creditors from seizing the assets inside your holding company.

Instead, creditors are limited to a lien on distributions—if the holding company doesn’t distribute profits, creditors may receive nothing.

For maximum protection, business owners should:

This arrangement creates what legal experts call a “firewall” between your personal wealth and business obligations.

Smart entrepreneurs use an “asset segregation” strategy by creating multiple LLCs under one holding company. Each valuable asset—real estate properties, equipment, intellectual property, and investments—gets its own dedicated LLC.

This approach means that only a specific LLC is at risk if one asset is sued. The Florida limited liability company has become the preferred entity for asset protection, replacing traditional corporations.

Consider this structure:

Holding Company LLC (owns everything)

This multi-layered approach creates barriers against liability. If someone sues your Operations LLC, your real estate and intellectual property remain protected in their separate entities.

Florida business owners can establish specialized trusts that work alongside their holding company structure for enhanced protection beyond LLCs. These trusts provide another layer of asset protection and offer additional benefits.

Florida asset protection trusts can be particularly effective when:

The most common types include irrevocable trusts and land trusts. Florida holding companies can own real estate through these trust arrangements, adding extra protection layers.

When properly structured, these trusts can help shield real estate investments from personal lawsuits targeting the business owner.

Business owners should consult an asset protection attorney to ensure that trust documents complement their LLC structure.

Trust strategies work best when implemented before any legal threats materialize. Courts may invalidate transfers made to avoid existing creditors.

Confused by complex business laws and tax rules? Making the wrong move can lead to costly mistakes. Let Mary Conte Law handle the legal details of your holding company so you can focus on growing your business. Get in touch now!

If you’re ready to get started, call us now!

Setting up a holding company requires careful planning to maximize protection and tax benefits.

The following mistakes can significantly impact your holding company’s effectiveness and potentially expose you to unnecessary risks or costs.

One of the most critical errors when establishing a holding company is failing to maintain separate finances.

Mixing personal and business funds can pierce the corporate veil, eliminating the liability protection that motivated your holding company creation in the first place.

Business owners should:

This separation isn’t just good practice—it’s essential for maintaining the legal protections a holding company provides.

Without it, courts may determine that the holding company is merely an extension of yourself, rendering the protective structure ineffective.

Many entrepreneurs rush to establish their holding company without fully understanding the tax implications of different business structures.

The step-by-step process for creating a holding company should include careful consideration of tax consequences.

Different structures provide varying benefits:

The optimal structure depends on your specific circumstances, investment goals, and growth plans.

Consulting with a tax professional before formation can save thousands in unnecessary tax burdens and prevent costly restructuring later.

A holding company requires ongoing attention to compliance matters. Many owners set up the initial structure but then neglect regular maintenance requirements.

Essential compliance activities include:

Failing to meet these obligations can result in penalties, loss of good standing, or even administrative dissolution. This negligence can invalidate liability protection and create tax complications.

Some states also impose personal liability on owners for debts incurred during periods of non-compliance. Set calendar reminders for all filing deadlines and consider using compliance services to manage these requirements.

Mary Conte Law offers legal guidance on selecting the optimal legal structure for your holding company.

Their team specializes in Florida business formation with particular expertise in LLCs and corporations, which are the most common structures for holding companies.

The firm helps clients with crucial formation steps, including:

Their attorneys also provide detailed tax planning advice. This includes guidance on how holding companies can be structured to minimize tax burdens while maintaining legal compliance with state and federal regulations.

Mary Conte Law specializes in personal asset protection strategies that shield business owners from potential liabilities. Their attorneys design holding company structures that legally separate valuable assets from operational businesses.

This separation creates a protective barrier that can:

The firm’s attorneys carefully analyze client assets and develop customized protection plans.

They ensure proper documentation and maintenance of corporate formalities to prevent “piercing the corporate veil” issues that could compromise asset protection.

Mary Conte Law provides tailored consultation services for entrepreneurs and business owners considering a holding company structure.

Their approach begins with a comprehensive assessment of the client’s specific needs, assets, and long-term business goals.

While hiring an attorney to form a holding company in Florida is not legally required, working with Mary Conte Law can help you avoid costly mistakes.

They ensure that formation documents are correctly prepared and filed, corporate formalities are maintained, and the holding company structure effectively achieves the client’s protection and tax planning goals.

Starting a holding company sounds simple—until you hit hidden fees, legal hurdles, and tax issues. Don’t let these challenges slow you down. Mary Conte Law helps you set up your business the right way. Book a strategy call today!

What is a Holding Company, and How Does It Work?

A holding company is a business entity that owns assets, stocks, or other companies but does not engage in operations itself. It primarily protects assets, minimizes liability, and optimizes tax benefits. In Florida, holding companies often manage real estate, businesses, or investments through subsidiaries.

What Are the Steps to Set Up a Holding Company in Florida?

To set up a holding company in Florida, follow these steps:

Do I Need an LLC or a Corporation for a Holding Company?

The best structure depends on your business goals:

Most Florida holding companies are formed as LLCs due to their ease of management and tax benefits.

What Are the Tax Benefits of a Holding Company in Florida?

Florida does not have a state income tax for individuals, and LLCs benefit from pass-through taxation, meaning profits are taxed only at the owner’s level. Corporations are subject to the federal 21% corporate tax rate.

What Are the Costs of Forming a Holding Company in Florida?

The initial and ongoing costs include:

Can a Holding Company Own Real Estate in Florida?

Yes, a holding company can own and manage real estate assets in Florida. Many real estate investors create LLC holding companies to separate properties into subsidiaries, reducing liability risks and enhancing tax efficiency.

How Do I Keep My Holding Company in Good Standing?

To maintain compliance in Florida:

Latest Post

October 18 2025

Probate in Seminole County: What Central Florida Families Should Expect in 2025

When a loved one dies in Seminole County, families suddenly have to deal with the legal process...

October 18 2025

Correcting Errors on Recorded Deeds in Seminole County (Corrective Deed & Re-recording Guide)

Sometimes, property owners in Seminole County spot errors on their recorded deeds. These mistakes...

October 18 2025

Affidavit of Continuous Marriage & Name Changes on Title (Florida Homeowners Guide)

Florida homeowners often encounter confusing paperwork when they get married, get divorced, or...